How private money financed a YouTube documentary

Also, is Instagram and TikTok coming to TV; is there enough ad money to go around? Plus C4 launches a new YouTube comedy brand.

This week, I’ve included the following:

How private money financed a YouTube documentary

Will Instagram and TikTok try to grab some of the connected TV audience

Is there enough ad money to go around

Channel 4 launches a new YouTube comedy brand

Some examples of new generation companies getting into the TV/film/creator hybrid space.

As always, send me a DM or drop a comment below if you’ve got thoughts you’d like to share:

—

Submit your entries to the Indielab Innovation Awards 2025

To mark 10 years of championing indie talent, Indielab is launching the brand-new Indielab Innovation Awards, taking place on the evening of GrowthLab London, 13 November 2025.

These Awards will celebrate the boldest and most original content and creators shaping the future of UK TV and digital-first storytelling. With categories including Best Drama, Best Documentary, Creator of the Year, and YouTube Channel of the Year, there’s a spotlight waiting for you.

👉 Be part of this milestone event - enter now

—

Privately funding a documentary to reach audiences via YouTube

Trevor Milton was the founder of a company called Nikola, which was involved in the development of electric and hydrogen powered trucks. He was convicted of fraud and sentenced to prison in 2023, and went on to be pardoned by President Trump in March this year.

He’s now released a feature documentary on his YouTube channel, which has had 24m views in the first four weeks of it being published.

Mark Soldinger - now of Skytoucher Films, ex founder and CEO of Firecracker - is the director, and he said on LinkedIn that it was a strategic decision to premiere it on YouTube due to the potential for audience reach.

The above article quotes Trevor Milton saying that using YouTube to publish the documentary ensured it could achieve ‘unrestricted global access’. He goes on to say:

For years, I’ve been silent—forced to sit back while the media, opportunists, and corporations ran wild with their version of my story. Today, that silence ends. I want people to watch the film, think for themselves, and finally get the full picture.

If ads had been running since it was published, it would have generated around £60k net of YouTube share in the first four weeks, depending on the volume of ads within the 110 minute documentary. Plus, it isn’t clear what paid promotional activity as well as the PR campaign have been run to support the film’s release.

Another point of interest about this approach is what - if anything - it does to the production budget. While the credits and production values demonstrate that this is a properly resourced feature doc, self financing often means that costs can be lowered by the removal or reduction of things like multiple viewings and so on. Whether this is the same when a documentary is privately financed may depend on the individual circumstances of each project.

There does seem to be an emerging trend of famous or infamous people looking to use documentary as a mechanism to get their own perspective out there and take greater control of their own stories and the issues they care about.

Therefore, YouTube rather than a streamer or broadcaster is a natural platform for these types of documentaries: it enables a direct relationship with global audiences; distribution and monetisation can be controlled; and the broadcaster/streaming gatekeeping process can be bypassed.

Another area we’ve seen some of this type of self or privately financed documentary production and distribution is by talent in fields such as sports or music. An example previously shared is Jude Bellingham’s documentary that was created by his own production company and published via his own social channels:

And there are other instances where individuals are looking to tell their own stories and take control of their narrative in a similar manner. One to keep an eye out for in the future.

Convergence marches on: Instagram & TikTok both want the TV

The Information has reported recently that both Instagram and TikTok are developing apps that optimise their content on the TV set. This isn’t either company’s first rodeo when it comes to TV; TikTok had a TV app however it no longer exist, while Instagram had a standalone app called IGTV over three years ago as an experiment in longer form videos up to 60 minutes.

This shift matters to the TV production sector for several reasons. Firstly, it is yet more evidence that the high value battle ground is the TV set, with yet more competition for audiences’ attention. This creates both opportunities for TV producers to find eyeballs via these apps, as destinations in their own right as well as potential marketing opportunities to get users to watch the full length show or film on the TV.

It also signals an opportunity as well as a warning klaxon around advertising. Which leads on to the next point…

A finite amount of advertising money

When you work in TV production, the world of advertising can be a bit of a mystery with a fairly common assumption there is an endless supply of advertising at a price point that remains somewhat static.

However, neither of these things are true. The ad market is hugely varied, fluid and complex, and there is also a limit on the number of companies & brands who want to spend on advertising: so yes, while new companies can enter the market for advertising, their demand for ad slots isn’t dictated by the growing supply of content - instead, if there aren’t advertisers to buy the ad slots, they simply go unfilled. And the volume advertisers want to purchase can go up and down depending on their own company’s position as well as geopolitical and economic conditions; so when there is a recession or high inflation, companies often rein in spending which means less advertising. Equally, people might stay in doors and watch more TV, so ad spend on TV might go up and down in other areas like cinema. The price points that advertisers pay for ad slots also fluctuates, and is influenced by the content genre, geographical territory and audience demographics, plus also how much inventory is out there can push price points down. On top of all of that, different types of advertising are valued in different ways, and companies’ ad strategies are heavily influenced by what they are trying to achieve: is it Google AdWords delivering results? Social? Billboards? Cinema? Print? TV?

The reason for explaining all of this is that there is fierce competition for share of the ad market, and thanks to convergence, this is cutting across all sorts of media and territories which previously were in relatively distinct markets.

To give some examples, there is the big growth of FAST channels (free ad supported TV such as Tubi), and yet when you see articles like the one below which includes phrases such as ‘publishers struggle with unfilled inventory’, then these could be interpreted as amber lights flashing on the dashboard:

The piece is worth reading as it explains how especially in the US, lots of connected TV ad inventory goes unfilled because there are so many FAST channels and libraries with low viewers so no advertiser wants to advertise with them. Then conversely, there are FAST channels with lots of viewers but low CPMs and even in this case, there are too many ad slots than the number of advertisers looking to buy at this price point.

In the UK, there is the fairly mature and sophisticated broadcaster ad funded VOD market, and as mentioned a few weeks ago, you can see the advertiser market hotting up here where commercial broadcasters try to grab more of the digital ad market - either by taking share off other video platforms and streamers or alternatively, by attracting those who buy digital advertising campaigns (such as Google or Meta), but haven’t as yet been the market for video advertising.

Thanks to Ian Whittaker for sharing Jacqueline Freeman’s piece below which outlines what lessons the UK TV ad market can offer to New Zealand:

She includes the following:

New Zealand often looks to the US for media thinking. But when it comes to television, the US is the exception - not the rule. US TV faces legacy issues: high ad loads, fragmented measurement, declining trust, pay-TV dominance and a deteriorating viewer experience.

And goes on to make the point how the UK’s market is different to the US, for example:

Trusted public and commercial broadcasters

Tighter regulation and lighter ad loads.

This is something I’ve mentioned previously for both those inside and outside of the US to be aware of - which is that the US TV and catch up VOD experience is very different to the rest of the world.

I can’t help wonder if the UK’s better TV user experience in terms of lower ad loads as well as comprehensive catch up VOD services could be an important lesson for US networks - or perhaps due to market complexities and disruption that ship has long since sailed?

Then there is Amazon and its drive to grab as much of the video advertising pie as possible. Plus YouTube’s strategy to push up quality and reliability on the platform again to try to snaffle more of the premium video ad market. And now both Instagram and TikTok are looking to get people to watch their content on the TV, although their ad experiences aren’t in the premium video space (although another one to watch out for).

Never mind all the other advertising opportunities out there - podcasting for example, but also games which thus far has not made much inroads into the ad market for a variety of reasons.

Not only is a battle raging that is important to be aware of, there is also an opportunity for producers. Advertisers like high quality premium content that can attract specific audiences, and therefore being able to produce this content is a valuable skill - either via commissioned output or in the direct to consumer market.

However, there is a sting to be aware of if you are in the direct to consumer market: it is risky to rely too much on ad inventory being sold at a particular price, as a) the inventory might not sell due to the volume of ad slots out there and b) even if it is sold, it might not be at the price you’d planned for.

And so, one way to hedge against this is to have multiple revenue streams to reduce the dependency on ad money - so branded partnerships, subscriptions, merchandising, events and so on.

Channel 4 launches new comedy channel with Strong Watch Studios

Another interesting announcement this week, which is yet another indication of broadcasters increasingly treating YouTube as a destination in its own right for content, audiences and monetisation, rather than as a marketing channel to drive audiences to linear TV or catch up VOD services.

Channel 4 has announced they are going to launch a new original comedy brand on YouTube. Called ‘A Comedy Thing’, it will publish a weekly long form show which at first will be focussed on stand up comedy, and then use TikTok and Instagram for clips to promote the full YouTube episodes.

They are working with Strong Watch Studios - Thom Gulseven and Ben Powell-Jones’ company. They both have long pedigrees in making great entertainment and comedy content that they call ‘digital broadcast’, which is the gap between legacy TV formatting and the world of digital publishing. Or a they describe it as:

… a gap we’re totally obsessed with, and one that uses the best of two industries we love.

This is another instance demonstrating the emerging broadcaster strategy of treating YouTube as a platform for originals and a home for evergreen channels around particular genres. So in broad terms, despite flurries of innovation and experimentation going back 20 years, broadcasters and TV IP owners had settled into using YouTube as a place to package up and distribute existing shows - so in Channel 4’s case, it has multiple genre YouTube channels such as Channel 4 Comedy which has lots of archive shows, compilations, clips and the like.

While there are some longer running strands for originals - Comedy Blaps most notably - the Channel 4.0 strategy has shown a path to build long-lasting channels on YouTube that can then attract an audience that is receptive to new original shows.

Sacha Khari, Channel 4’s Head of Digital Commissioning has said that in the longer term their ambition is to make podcasts as well. Demonstrating how successful brands can be platform neutral and work across multiple content formats to reach audiences.

A few other points to note: it is interesting that this instance is narrowly targeted at a genre (comedy) rather than Channel 4.0 which is focussed on the youth demographic. At launch it sounds like it is focussed on standup rather than sketch comedy - possibly a great route for regular new content that is cheaper to produce than scripted. And lastly, I don’t know anything about the shape of the deal, but I’d be curious whether it is a straightforward commission with fees paid to the talent, or if there is any revenue and IP sharing going on here.

The channel is due to launch on July 21, so one to watch out for.

Companies stepping into the hybrid creator/TV/film market

There have been a couple of company launches in the last month or two I thought worth sharing, as they showed a future trend of new and different types of businesses for our converged world.

The first is a company called Unicorn, which has been launched as both a talent agency as well as a video production studio.

The Publish Press: Unicorn Launches to Manage Creators and Produce Their IP

Axios: Unicorn launches to help creators build YouTube shows

The idea is that Unicorn will both represent creators as well as produce short and long form shows for those on the company’s roster. They say the business model will see the company and the creators split show IP and revenues 50/50 from sales, brand deals, advertising, products and subscriptions. The founders Scott Dunn and Chris Gera have a background in building channels and producing content for companies like Buzzfeed, and are quoted as saying:

If you're only overseeing one side of talent management or IP, it's very opaque and doesn't work in tandem with one another… Bringing it all together is a unique way to solve a lot of these problems and make it feel team-oriented.

The second company is Further Adventures from YouTube veteran Steve Beckman and producer Ben Stillman, will work with independent filmmakers and creators to develop and produce new IP and projects.

They are working with filmmakers such as Walter Thompson-Hernández, whose short If I Go Will They Miss Me won the Sundance Grand Jury Prize, and Ramzi Bashour, who also has received support from Sundance Labs.

The company is also working with Andrew Rea, whose Binging With Babish YouTube channel has 2.9bn views and 10.4m followers, plus he does live events, and has his own cookware range.

For TV producers, there are two reasons to flag these announcements. Firstly, you can see how increasingly in the online arena, companies and domains are merging as part of this process of convergence. Where previously talent agencies might more frequently be separate to production studios, this demonstrates the trend to blend content production with all other aspects of a creator’s business.

And secondly, this also shows the common thread with many (if not all) of the creator examples I’ve been sharing: these businesses all have multiple revenue streams across a whole myriad of channels, products and services, and together they build up to a potentially lucrative scalable business. Crucially, these new types of businesses are conceptualised and run in a flatter, more fluid and integrated manner rather than the more traditional siloed and hierarchical approach of TV production companies and broadcasters. Some something a little like this:

These types of new entertainment operations are demonstrating opportunities for TV producers and production companies, however it is crucial to adapt both in approach as well as internal structures to be able to thrive in this world.

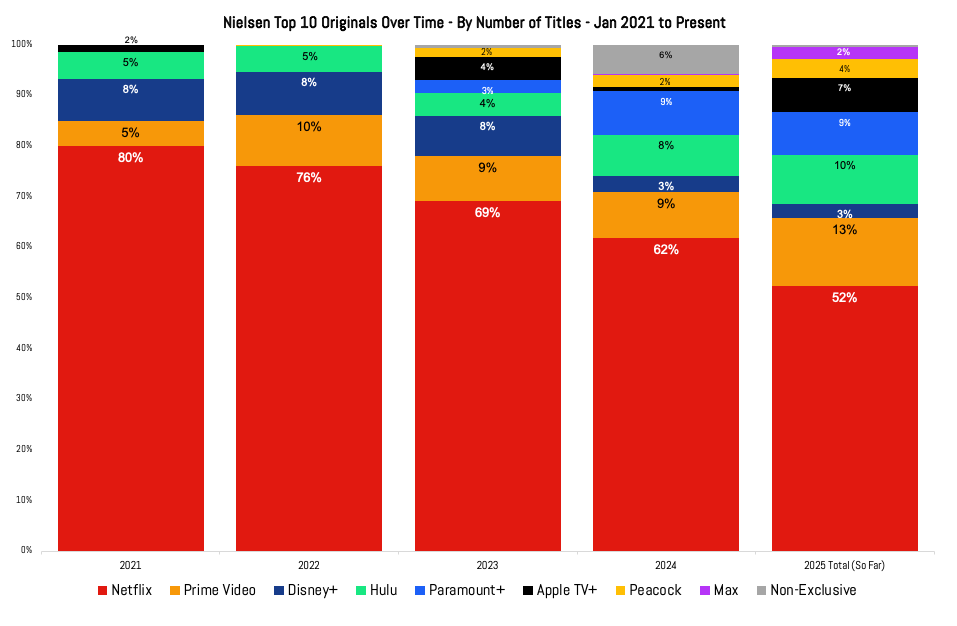

Graph of week/month/year

shared this corker of a graph this week, which is part of a deep dive he’s done into Netflix's share of titles in Nielsen’s top ten originals chart in America, going back the last four years.

The full post is worth reading, as it demonstrates that yes, in the US at least, the streaming wars are getting more competitive, however as always, his writing reflects the nuance and complexity of this market. And the above is about the number of titles in the top 10 - so release patterns impact this, and also doesn’t reflect share (although he’s done that too in the post below), say where one big juggernaut title like Squid Game gets lots of views. Plus of course this doesn’t take into account how the global streamers on this list view ROI; in other words do they value performance in certain territories which isn’t reflected in these US numbers.

Even so - the ones that stood out as well as Netflix include how Disney has stuttered in the last few years, that Paramount has been having a good run, and Max has finally made an appearance.

Find out more about me and the purpose of this newsletter, say hi via email hello@businessoftv.com, or connect with me on LinkedIn.

24 million views but no comments or likes?

.. Great Post - outstanding in fact .. but intimidating seen from a filmmakers perspective.

i can’t deal with this stuff .. too old school.. haha - I give a fuck where my stuff gets screened.. that’s ’producer turf .. (the reader or audience is who I have to ‘Know inside Me’ in order to ‘speak to them) - do ya think I want that Producer getting their creative camel nose near the Directors Tent ?

The ‘hunt for myself is finding an advocate who ‘walks these waters.. (cuz i is witless re Business End) I need someone who know’s / recognizes when they come upon a ‘major league blueprinted property’ with great merit / action drama story & loaded with ‘intangible opportunity .. comes with major bonus points - will require approx 30 shoot day’s in Providenciales TCI - the potential ‘Product Placement is off planet blowaway.. Story Outline that ‘visually sizzles - Design/Written to Budge 1/4 of ‘Fool’s Gold’

btw i had a looksee at that Trevor - Docu .. have to say its wake-up call confrontational to myself ! I knew nothing of this ‘story.. or ‘reality .. zero - but i know when i’m seeing unlimited production budget - every Dept - Feature Level through & through.. even Top Ad Agency - Various ‘Specialty Connections..

I probably would burn 2 hours just ‘following up with this Post ‘ It’s ‘Loaded !

🦎🏴☠️🎬